Insurance in India – Complete Guide to Types, Plans & Coverage

Insurance in India 2026 – Complete Guide to Types, Plans & Coverage

Insurance is one of the most misunderstood yet essential financial products in India. While many people understand the concept, very few actually have adequate coverage for themselves and their families.

Whether it’s protecting against unexpected medical bills, securing your family’s financial future after your death, or protecting your assets, insurance provides peace of mind that money alone cannot buy.

In this comprehensive guide, I’ll explain everything about insurance in India, including different types, how to choose the right plan, and where to buy.

What is Insurance?

Insurance is a financial contract between you (policyholder) and an insurance company where:

- You pay a premium (regular payment)

- The insurance company pays when an insured event occurs

- The payment is called a “claim” or “benefit”

Key Insurance Principle:

Risk Transfer: You transfer your financial risk to the insurance company in exchange for a small premium.

How Insurance Works:

Example: Life Insurance

- You pay ₹400/month premium

- If you die, insurance company pays ₹1 crore to your family

- This gives your family financial security

Types of Insurance in India

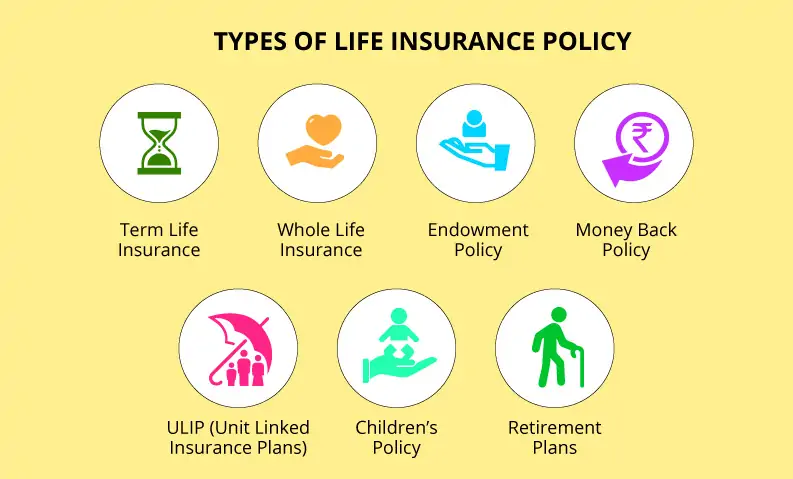

1. Life Insurance

What It Covers: Financial protection in case of death Who Needs It: Earners with dependents Types: Term, Whole Life, Endowment, ULIP Premium: ₹300-1000/month for ₹1 crore Claim Amount: Lump sum to beneficiary

Best For:

- Young families

- Breadwinners

- Ensuring family doesn’t face financial crisis

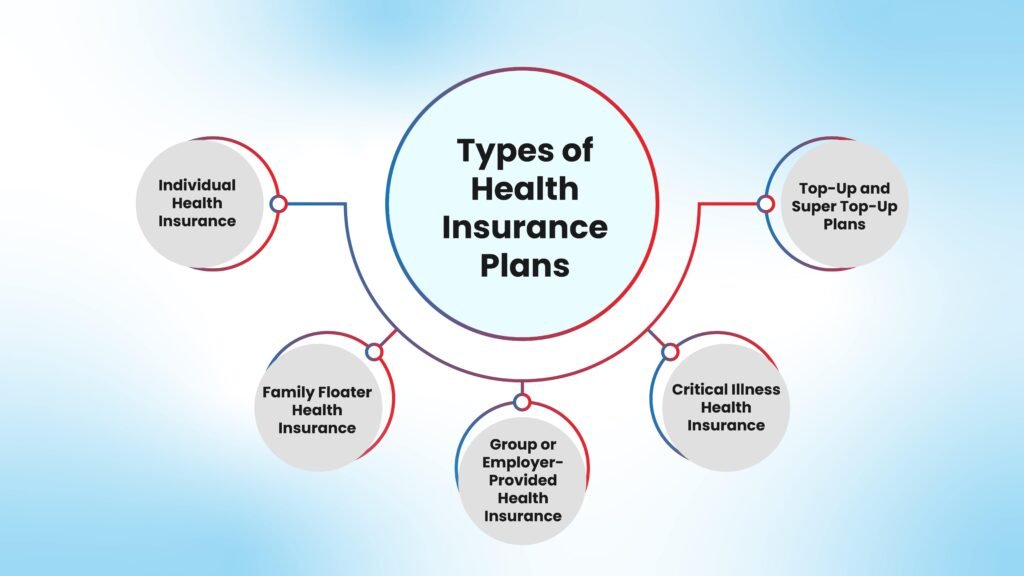

2. Health Insurance

What It Covers: Medical expenses (hospitalization, surgery, treatment) Who Needs It: Everyone (especially families) Types: Individual, Family Floater, Group Health Premium: ₹2,000-8,000/year for family of 4 Coverage: ₹5 lakh to ₹1 crore

Best For:

- Protection from medical inflation

- Planned and emergency healthcare

- Reducing out-of-pocket medical expenses

3. Car Insurance

What It Covers: Vehicle damage, liability, third-party claims Who Needs It: All car owners (mandatory by law) Types: Third-party, Comprehensive Premium: ₹5,000-15,000/year Coverage: Varies by plan

Best For:

- Legal compliance

- Protection against accidents

- Third-party damage liability

4. Home Insurance

What It Covers: Home structure, contents, liability Who Needs It: Homeowners Types: Fire, Burglary, Flood, Comprehensive Premium: ₹3,000-8,000/year Coverage: Up to property value

Best For:

- Protection against natural disasters

- Theft/burglary

- Accidental damage

5. Travel Insurance

What It Covers: Medical, baggage, cancellation, trip delay Who Needs It: Domestic and international travelers Premium: ₹500-2,000 per trip Coverage: Up to ₹1 crore

Best For:

- International travel

- Medical emergencies abroad

- Baggage protection

- Trip cancellation

6. Critical Illness Insurance

What It Covers: Major illness diagnosis (cancer, heart attack, stroke) Who Needs It: Working adults Premium: ₹1,500-3,000/year Benefit: Lump sum on diagnosis

Best For:

- Treatment financing

- Replacing lost income during recovery

- Medical cost coverage

Life Insurance Types Explained

Term Insurance (Best Value)

- Pure life insurance

- No investment component

- Lowest premium

- Maximum coverage

- No maturity benefit

- Best for: Young families

Example: ₹1 crore coverage = ₹400/month for 30-year-old

Whole Life Insurance

- Life-long coverage (up to age 100)

- Higher premium than term

- Includes some savings

- No maturity benefit (unless policy matures)

- Best for: Lifelong protection

Example: ₹1 crore coverage = ₹3,000-5,000/month

Endowment Insurance

- Combined insurance + investment

- Premium for fixed period

- Maturity benefit at end (return of premium)

- Lower coverage than term

- Best for: Long-term saving

Example: ₹50 lakh coverage = ₹5,000-8,000/month

ULIP (Unit Linked Insurance Plan)

- Insurance + market-linked investment

- Premium invested in funds

- Variable returns

- Tax benefits under Section 80C

- Best for: Long-term wealth + protection

Example: ₹50 lakh coverage = ₹4,000-6,000/month

Health Insurance Plans

Individual Plans

- Coverage for one person

- Premium based on age and health

- Best for: Single adults

- Premium: ₹2,000-5,000/year

Family Floater Plans

- One sum insured for entire family

- Premium shared across family

- Most cost-effective

- Best for: Families of 3+

- Premium: ₹3,000-8,000/year

Group Health Insurance

- Provided by employer

- Employer pays premium

- No medical underwriting needed

- Best for: Employed individuals

- Premium: Company-paid

Senior Citizen Plans

- Specifically for 60+ years

- Higher premiums

- Adjusted coverage

- Pre-existing condition coverage

- Best for: Elderly parents

Insurance Claim Process

Step-by-Step Process:

Step 1: Notify Insurance Company (within 30 days)

- Call customer service

- Provide policy number

- Give incident details

Step 2: Submit Documents (within 10-15 days)

- Claim form (filled and signed)

- Original policy document

- Identity proof

- Relevant documents (medical bills, death certificate, etc.)

Step 3: Verification (2-4 weeks)

- Company verifies information

- May request additional documents

- Conducts investigation if needed

Step 4: Claim Assessment

- Documents reviewed

- Eligibility determined

- Amount calculated

Step 5: Approval & Payment (5-7 business days)

- Claim approved

- Money transferred to bank account

- Claim settled

Average Claim Settlement Time:

- Quick claims: 5-10 days

- Complex claims: 2-4 weeks

- Maximum: 30-90 days

Factors Affecting Insurance Premium

Life Insurance Premiums:

- Age – Biggest factor

- Younger = Lower premium

- 25 years: ₹300/month

- 35 years: ₹600/month

- 45 years: ₹1,500/month

- Health Status

- Good health = Lower premium

- Medical conditions = Higher premium

- Smokers = 2x higher premium

- Coverage Amount

- Higher coverage = Higher premium

- ₹50 lakh = ₹200/month

- ₹1 crore = ₹400/month

- Tenure

- Longer tenure = Lower premium

- But total payment may be higher

Health Insurance Premiums:

- Age

- 18-30: ₹2,000-3,000/year

- 31-40: ₹3,000-4,500/year

- 41-50: ₹5,000-7,000/year

- 50+: ₹8,000-15,000/year

- Sum Insured (coverage amount)

- ₹5 lakh = ₹3,000/year

- ₹10 lakh = ₹5,000/year

- ₹20 lakh = ₹8,000/year

- Pre-existing Conditions

- Loading (extra premium)

- Varies by condition

- Increases with age

- Claims History

- No claims = Normal premium

- Previous claims = Higher premium

Read More: Personal Loans in India – Complete Guide to Instant Approval & Best Rates

How to Choose the Right Insurance

Life Insurance Decision:

Step 1: Calculate Coverage Need

- Annual expenses × 20 = Base amount

- Add home loan balance

- Add children’s education goals

- Add retirement funds needed

- Result = Ideal coverage

Step 2: Choose Type

- Young + Budget? → Term Insurance

- Long-term + Wealth? → ULIP

- Lifelong + Security? → Whole Life

Step 3: Select Tenure

- 20-30 years recommended

- Should cover till age 60

Step 4: Compare Rates

- Visit PolicyBazaar.com

- Check 5-6 insurers

- Compare premium for same coverage

Step 5: Apply

- Online application

- Medical tests (if required)

- Approval in 2-3 weeks

Health Insurance Decision:

Step 1: Assess Coverage Need

- Individual? → Minimum ₹5 lakh

- Family of 4? → Minimum ₹10 lakh

- Multiple family members? → Minimum ₹15 lakh

Step 2: Choose Type

- Individual living alone? → Individual plan

- Family? → Family floater (best value)

- Senior citizen? → Senior citizen plan

Step 3: Compare Plans

- Visit Policybazaar or Policychest

- Compare network hospitals

- Check coverage details

- Review claim settlement ratio

Step 4: Check Key Features

- No waiting period for emergency

- Pre-existing condition coverage

- Room rent limits

- Co-payment clauses

- Network hospitals in your city

Step 5: Apply

- Online application

- Health declaration

- No medical test needed (usually)

- Approval in 3-5 days

Best Insurance Companies in India 2026

Life Insurance Companies:

- HDFC Life – Most trusted

- ICICI Prudential – Wide range

- SBI Life – Affordable

- Max Life – Good riders

- Kotak Life – Customer service

- Bajaj Life – Competitive rates

Health Insurance Companies:

- HDFC Ergo – Largest network

- Apollo Munich – Best claim settlement

- ICICI Lombard – Good coverage

- Aditya Birla Health – Affordable

- Bajaj Allianz – Wide range

- Star Health – Specialized plans

Read More: Personal Loans in India – Complete Guide to Instant Approval & Best Rates

Common Insurance Mistakes to Avoid

❌ Mistake 1: Buying Too Low Coverage

- Most people buy insufficient coverage

- Insurance is just basic protection

- Solution: Calculate properly

❌ Mistake 2: Not Disclosing Medical History

- Hiding pre-existing conditions

- Company rejects claim

- Solution: Always disclose truthfully

❌ Mistake 3: Not Reviewing Policy

- Life changes (marriage, child, home)

- Coverage becomes inadequate

- Solution: Review yearly

❌ Mistake 4: Delaying Purchase

- Every year, premium increases significantly

- Age 25: ₹300/month vs Age 40: ₹1,200/month

- Solution: Buy early while young

❌ Mistake 5: Wrong Insurance Type

- Buying investment-heavy when need pure protection

- Wrong coverage type for needs

- Solution: Match insurance to need

❌ Mistake 6: Not Updating Beneficiary

- Old beneficiary after marriage

- Benefit goes to wrong person

- Solution: Update after life events

Insurance FAQs

Is insurance mandatory in India?

Car insurance is mandatory by law. Others are voluntary but highly recommended.

How much life insurance do I need?

Generally 10-15x annual income, or calculate based on family’s financial needs.

Can I get insurance with pre-existing condition?

Yes, but with higher premium and possible waiting period for coverage.

How quickly can I get insurance approved?

Term insurance: 2-4 weeks. Health insurance: 3-5 days. Fintech: Few hours.

Is insurance premium tax deductible?

Life insurance: No. Health insurance: Yes, up to ₹25,000/year under Section 80D.

What happens if I don’t pay premium?

Grace period of 30-45 days. After that, policy lapses but can be revived.

Conclusion

Insurance is not an expense, it’s an investment in peace of mind and financial security. Whether it’s protecting your life, health, home, or vehicle, insurance ensures you and your family face adversity without financial ruin.

Action Steps:

- Calculate your insurance needs

- Compare policies on PolicyBazaar

- Choose appropriate coverage

- Apply online today

- Get approved within days

- Start your peace of mind

Remember: The best time to buy insurance was yesterday. The second-best time is today.